America's 'entitlement' system (medicare & social security totals $27 K per year, average 12 years benefit payout, 4 paid for, 8 NOT) is a PONZI scheme that WILL collapse shortly because the math

as EL GATO MALO shows, is stunning & the system cannot be supported 'AS IS'; this is a PONZI we have to 'get out of' NOW but how? 270,000 $ unfunded per person! how can it stay afloat?

‘we can then sum that which was paid in over 45 years of career and that number is $117,205, not an insubstantial chunk of change, but also not nearly enough to fund the benefits being paid out. in fact, it’s not even close.

the average medicare recipient is today taking out $15,722 per year.

the average social security recipient is taking out $11,312 per year.

that’s $27,084 total. see the problem?

with avg life span now at 77.28, the typical person is getting 12.28 years of benefits. but the cash they paid in only covers 4.33. there are 7.95 unfunded years at over $27k each and this cost is rising because social security and medicare both rise with inflation due to COLA (cost of living adjustment) and cost increases in medical care.

assuming a 3% COLA, the unfunded value per person is $267,172.’

‘after this recent piece about the impending failure of social security and medicare/medicaid that threatens to take down the whole of the federal budget some questions about the entitlement to take out because one payed in were raised.

this is, on the surface, something of a reasonable objection. however, as one digs into such a claim, it rapidly becomes apparent that such ideas cannot be supported because this was not a savings system, it was a ponzi system and that which was paid in was woefully insufficient to support that which winds up being taken out and therefore as the number claiming benefits inexorably rises due to longer lives and we therefore see fewer payors per recipient as the average years of benefits rise from 0 to 12 and change, the system cannot possibly support itself.

but it could have had it not been designed to fail.

let’s look.

first, the data here (from FRED, the st louis fed tool) only went back to 1974, but this, as it turns out, works well for this analysis as someone who went to work then at, say, 20 or 21 would have been born in 1953 or 1954 and thus be pretty much dead center of the boomer generation whose retirement is placing such stress on the system.

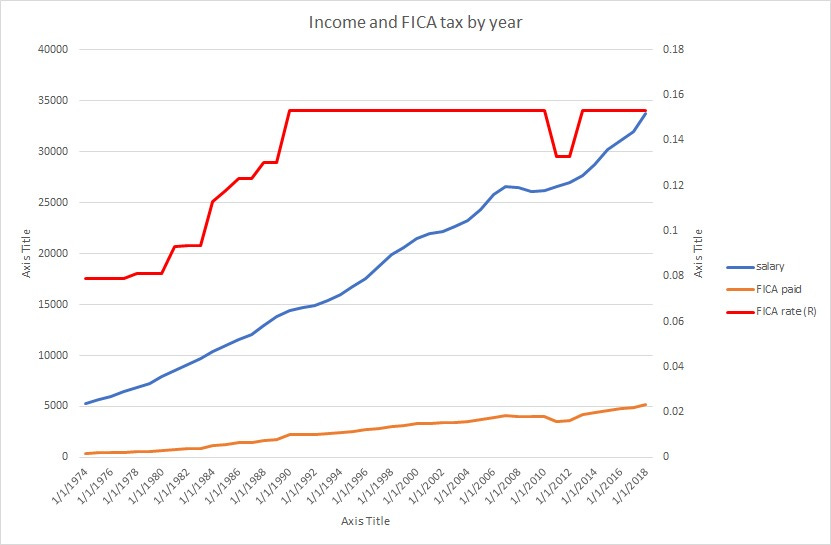

i took the median US salary by year and i multiplied it by the fully loaded FICA rate per year (individual plus employer contribution) which, it is worth noting, used to be much lower. it was only 7.9% in 1974 vs 15.3% today. from this we can calculate annual FICA payments into the system and aggregate them over a 45 year career to 65 which would end in 2018.

here’s the data in graphic form

we can then sum that which was paid in over 45 years of career and that number is $117,205, not an insubstantial chunk of change, but also not nearly enough to fund the benefits being paid out. in fact, it’s not even close.

the average medicare recipient is today taking out $15,722 per year.

the average social security recipient is taking out $11,312 per year.

that’s $27,084 total. see the problem?

with avg life span now at 77.28, the typical person is getting 12.28 years of benefits. but the cash they paid in only covers 4.33. there are 7.95 unfunded years at over $27k each and this cost is rising because social security and medicare both rise with inflation due to COLA (cost of living adjustment) and cost increases in medical care.

assuming a 3% COLA, the unfunded value per person is $267,172.

and therein lies the problem:

everyone paid in, but they did not pay in nearly enough to cover that which they are now taking out. it’s all being funded by current taxpayers and the amounts raised can no longer cover it and it’s just going to keep getting worse as the demographics continue to bite.

the payout to pay in is a 3.28 multiple.

clearly, that’s not going to work. you’d need a truly massive rise in the number of folks paying in.

the current (2022) median annual FICA payment is $6,193.

that means you need 4.4 payors per recipient to balance these books, but that number is under 3 and will drop to more like 2 shortly.

pretty difficult to see how this can possibly be made to balance without huge cost cuts.

this was a ponzi system from the beginning and we’re now getting to the ugly part.

but it didn’t have to be like this.

this happened because the state pooled all the money it took in, spent it on other stuff, and promised to put it back later. this is a convenient strategy for big spenders looking to pass the buck intergenerationally by effectively plundering the pension fund to splurge today and let tomorrow come once they are long gone (classic political gambit that it is) but it’s ponzi, pure and simple. there was never really any viable off ramp here save calamity.

but there could have been.

compound interest is an incredibly powerful force. $24 dollars paid for manhattan island seems like the real estate deal of the millennium, but if you had earned prevailing bond yields on that money from then until now, you’d have enough money today to buy all of new york state and every building in it. it’s serious stuff. and it works both ways as inflation also compounds like this. so you have a curve crossing problem where to keep buying power intact or rising, you need a return on your assets in excess of inflation (this is called “real” return).

and this could have happened.

if, instead of going into general governmental coffers to be spent by profligate politicians pretending there was no deficit by plundering the future, these monies had gone into personal savings accounts, things would be VERY different.

let’s take the simplest example: “risk free” savings by owning US bonds.

i used the one year rate to be conservative. now, the $117k paid in compounds (even despite a decade of ZIRP) to $200,532 by 2018, the time of retirement. and, once one does the math properly, it’s easy to see that if that money were actually yours, you’d be doing quite a lot better (but still not well enough as you’d run out of cash in 2026, 8 years into your retirement (assuming a 5.16% rate going forward, the period avg). this is a little unfair as a decade of near zero interest rates from 2008-17 greatly suppressed this overall income stream, but the numbers are the numbers, so that’s what we get. the shortfall at expected life end is now $198k, down from $267k. (all assuming 3% COLA)

BUT, you can not only eliminate this but invert it radically by finding higher rates of return using equities. if one had put the money each year into the S+P 500 (with dividends) then by retirement in 2018, the savings would have been $1,032,696 and that is sufficiently high that even once you start taking out every year for SS and medicare, the overall balance keeps rising even using only an 8% return assumption (far lower than the 12.1% over the past 45 years). also note that this return series is the opposite of a cherry pick as it started in 1974, a terrible year in which the S+P was down 26%, so that’s about as bad a start point as one could choose.

here’s the graph of savings over time for the 3 methods: (begin work, 1974; retirement 2018)

not exactly subtle, is it? and the question that will really boil your noodle if you stop to consider it is: might returns on equities been even higher over time if all this money had been available to fund private growth instead of being poured down gopher holes by the state? how much bigger might the economy as a whole be?

and this, of course, brings us to the real elephant in the room:

why on earth would anyone trust an entity as shortsighted, corrupt, and outright stupid as “the state” with the security of their retirement funds and health care? because like all ponzis, it’s great for a while, but one day, the music stops and everyone looks around and the whole world realizes at once that there are no chairs for anyone and the whole system collapses.

the state does not provide stability in such a case but rather the sort of mono-culture that makes systems unstable and takes them all down at once in a paroxysm of fiscal failure.

as ever, the mantra of “too important to be left to free markets/the people” is the most towering of lies. the comfort of one’s retirement is far too important not to be.’

The elderly and retired hard-working individuals who never took a cent from the government while providing for their families DESERVE our "entitlement" support. They earned it.

Not the young lazy good-for-nothings who contribute zero to society yet receive welfare, food stamps, and free, well, everything. Nor should illegal aliens receive ANYTHING from the U.S. or state governments. (They should be unceremoniously dumped onto the other side of the southern border.)

Paul, everyone on of us who have worked for years have paid into Social Security and Medicare, which is no different than the public pension funds that do the same for those who participate in them. The problem is it has been used as a slush fund for years by crooked corrupt politicians and given to people who DO NOT QUALIFY! These are not ENTITLEMENTS. As Kathleen commented, then you have the billions or trillions given to all these dead beats for their entire lives and now the illegal aliens are getting more than any American from our corrupt government to come in and destroy America. You are wrong on this one! Had we been able to invest those funds into 401(k) or other retirement plans than we could have managed this money without it being taken with no option for an alternative. SSI has never been mandated like the pension funds to maintain sufficient balances because the corrupt Federal Govenrment couldn’t keep their hands off of it. This is where the problem has been for years.